What Is Considered a Good Capitalization Rate? A Guide for Monterey County Investors

For savvy investors in Monterey County, a "good" capitalization rate isn't just one number—it’s a clear indicator of risk and potential reward. While a national range might be 4% to 10%, that figure changes dramatically based on a property's location, type, and the local market story.

A lower cap rate often points to a safer, more stable asset in a high-demand area like Carmel. Think of it as a blue-chip stock for your portfolio. A higher rate, on the other hand, can signal stronger immediate cash flow but usually comes with more risk, typical of faster-growing markets.

Decoding Cap Rates in the Monterey Bay Area

Think of a cap rate as a quick snapshot of your investment's earning potential if you bought it with cash. It's a simple calculation that measures the annual return from a property's income relative to its current market value. For serious investors focused on high-end properties in Monterey County, understanding the local context is crucial for maximizing ROI.

The numbers here tell a unique story about market stability, risk, and opportunity. In our premium coastal communities, expectations are different.

- Lower Cap Rates (3-5%): These are common in high-value areas like Carmel and Pebble Beach. A rate in this range shows strong investor confidence, high property values, and perceived safety. The return is steady, making the asset a stable, long-term hold for wealth preservation.

- Higher Cap Rates (6-8%+): You're more likely to see these numbers in growing areas like Salinas or South County towns such as Soledad and King City. A higher rate here compensates investors for different market dynamics, signaling greater potential for immediate cash flow.

This distinction is the key to building a successful portfolio strategy. An investor focused on preserving wealth might prefer the stability of a lower-cap-rate property in Pacific Grove. In contrast, an investor aiming for aggressive cash flow might target a higher-cap-rate multi-family unit in Salinas.

Monterey County Cap Rate Quick Guide

To give you a clearer picture, here’s a quick reference for what you can typically expect for different property types across our local market.

| Property Type | Typical Cap Rate Range | Key Investor Consideration |

|---|---|---|

| Luxury Single-Family | 3% – 4.5% | Stability and long-term appreciation are the primary goals, not immediate cash flow. |

| Multi-Family (4+ Units) | 5% – 7% | A balance of cash flow and growth, often seen as the workhorse of a portfolio. |

| Commercial Retail | 6% – 8% | Higher potential income but depends on tenant strength and the local economy. |

| Industrial/Warehouse | 5.5% – 7.5% | Growing demand but requires specialized management and tenant knowledge. |

This table illustrates the trade-offs. There's no single "best" option—only what's best for your specific financial goals and risk tolerance.

The Investor's Perspective on Risk and Reward

Ultimately, a "good" cap rate is one that aligns with your investment goals. It’s not just about chasing the highest number; it's about understanding the story behind that number. A high cap rate could be a fantastic opportunity, or it could be a red flag for a property with issues that demand significant time and management attention.

For the discerning property owner, the goal is to balance healthy returns with long-term asset preservation. The cap rate is a starting point—a diagnostic tool that helps us ask the right questions about a property's performance and potential.

Before we dive into the calculations, a solid grasp of the fundamentals is essential. For a complete primer, explore our detailed guide on what a cap rate is in real estate. This foundational knowledge allows you to make smarter, data-driven decisions that protect and grow your wealth in the unique Monterey County market.

A Practical Guide to Calculating Cap Rate

Figuring out your property's cap rate is a quick, powerful way to measure its performance. The formula is simple: Net Operating Income (NOI) divided by the Current Market Value. Think of this number as the potential rate of return you're getting from the investment, separate from any financing.

It’s like your property’s annual report card. It tells you exactly how well the asset generates income compared to what it’s worth today in the Monterey County market.

Breaking Down the Formula

The calculation boils down to two key numbers: what your property earns and what it’s worth.

- Net Operating Income (NOI): This is the total income your property brings in for the year (gross rent plus other income like parking fees) after you subtract all operating expenses. These expenses include property taxes, insurance, maintenance, and property management fees. Crucially, your mortgage payment is not included here.

- Current Market Value: This isn't what you paid five years ago. It’s the price a buyer would realistically pay for it in today's market, whether it's a luxury vacation home in Pacific Grove or a multi-unit building in Salinas.

To get your cap rate right, you first need a solid NOI figure. It's essential to understand how to properly calculate rental income because that number is the starting point.

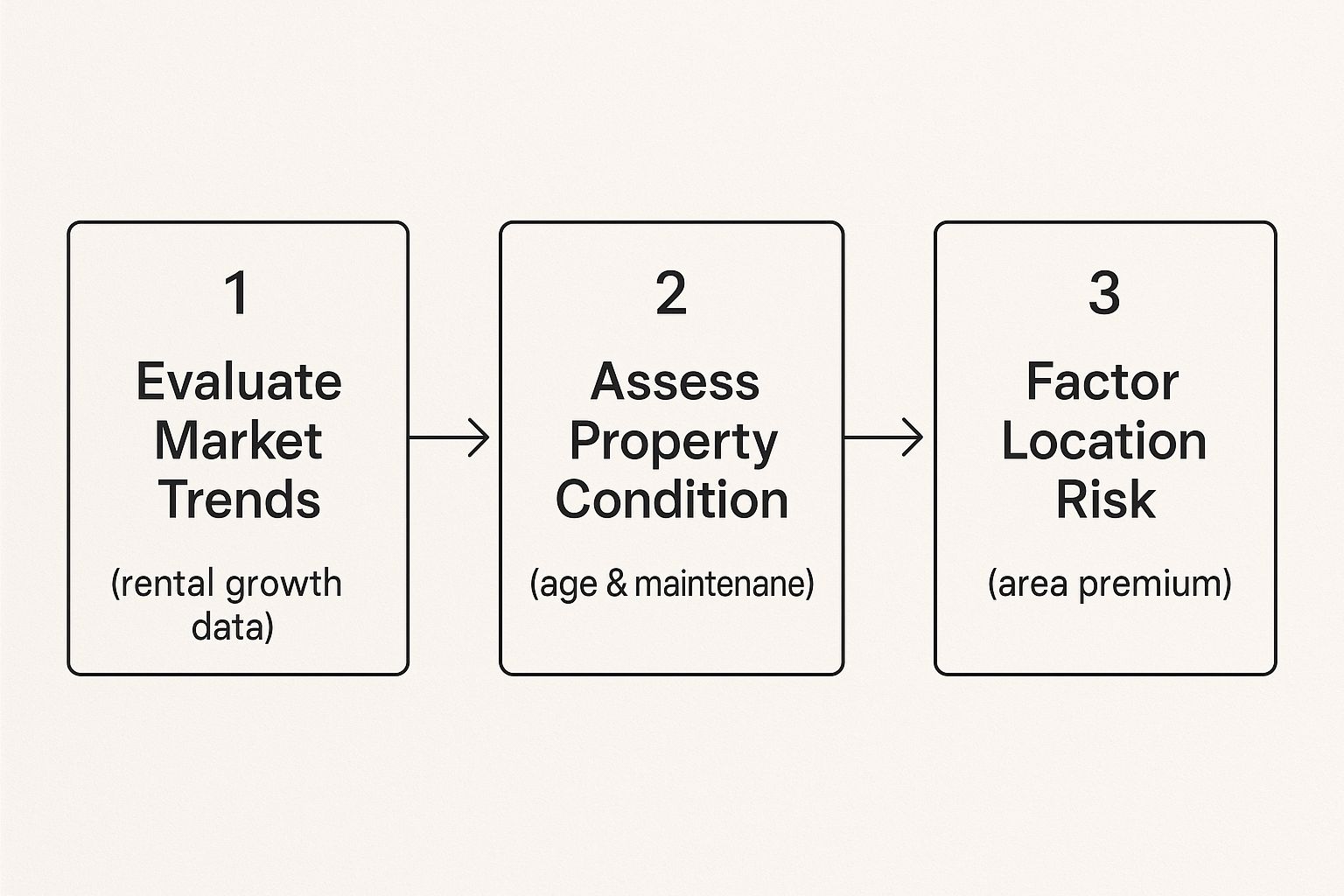

The visual below shows how market trends, property condition, and location-based risk all play a role in this calculation.

As you can see, a true cap rate analysis requires more than just plugging numbers into a formula; it demands a real feel for local market dynamics and your property's specifics.

A Real-World Salinas Example

Let's walk through this with a multi-family property in Salinas to see how it works in practice.

- Current Market Value: $1,200,000

- Annual Gross Rental Income: $90,000

- Annual Operating Expenses (taxes, insurance, maintenance): $30,000

Step 1: Find the Net Operating Income (NOI).

$90,000 (Gross Income) – $30,000 (Operating Expenses) = $60,000 (NOI)

Step 2: Calculate the Cap Rate.

$60,000 (NOI) / $1,200,000 (Market Value) = 0.05 or 5%

This 5% cap rate gives us a clean, standardized metric. We can now use it to compare this Salinas property against other investment opportunities, whether they're across town or across the country. It’s a vital tool for making smart portfolio decisions.

While cap rate is a fantastic indicator, it's always smart to look at it alongside other metrics. For another angle on your investment's health, check out our guide on how to calculate rental yield, which offers a slightly different perspective on performance.

Key Factors That Influence Local Cap Rates

Ever wonder why a property in King City can have a cap rate that looks completely different from one in Monterey? A savvy investor knows a cap rate isn't just a number—it’s a direct reflection of local market dynamics, the property's unique characteristics, and broader economic trends.

Understanding these influences is key to making smart decisions in our unique region. Several forces push and pull on property values and rental income, which in turn moves cap rates. For anyone investing in Monterey County, it’s critical to look past the basic formula and understand the story these factors tell about risk and opportunity.

Regional Economic Drivers

The economic health of our region plays a huge role. Monterey County's economy is a unique blend of agriculture and tourism, creating distinct patterns in rental demand and property values.

- Agricultural Strength: In Salinas and South County towns like Soledad and Gonzales, a strong agricultural sector provides a steady employment base. This consistency leads to stable rental demand for both multi-family and single-family homes, directly influencing their cap rates.

- Tourism Trends: Along the coast, from Monterey to Carmel, tourism is king. A strong tourist season boosts demand for short-term and luxury rentals, which can push property values up and lower cap rates, signaling what the market sees as a "safer" investment.

Property-Specific Details

No two properties are the same, and their individual traits are critical. Details about the asset itself have a direct impact on its Net Operating Income (NOI) and its perceived risk. A clear understanding of what goes into this figure is vital; for a deeper dive, check out our guide on what is net operating income.

Here are a few property-level factors to consider:

- Age and Condition: A recently renovated property in Pacific Grove with modern amenities will command higher rents and need less immediate maintenance. This justifies a lower cap rate. An older building with deferred maintenance will likely have a higher cap rate to compensate the new owner for the work ahead.

- Tenant Quality: A property with reliable, long-term tenants on solid leases is a less risky asset. That stability is attractive to buyers and often results in a lower, more stable cap rate.

What makes a "good" cap rate is closely tied to market conditions and risk. Back in the early 2000s, U.S. cap rates were commonly in the 8% to 10% range. But a long period of low interest rates led to "cap rate compression," pushing them down to 5% to 7% by 2006 as more money entered real estate. You can explore the history of real estate cycles to see how these trends evolve.

Comparing Cap Rates Across Property Types

Not all real estate is created equal, and neither are their cap rates. If you’re a serious investor in Monterey County, you know that what is considered a good capitalization rate depends on what you're buying. The risk and return profile of a multi-unit apartment building in Salinas is worlds away from a luxury single-family home in Carmel, and their cap rates tell that story.

Every property type has its own expectations for income stability, growth potential, and management needs. That's why comparing a commercial property to a residential one using the same cap rate lens can lead to poor decisions.

Risk and Stability Across Asset Classes

The main reason cap rates vary so much is the classic trade-off between risk and reward. Assets seen as safer and more stable—those with consistent tenant demand—usually have lower cap rates. Why? Because investors are willing to pay a premium for that peace of mind and long-term security.

- Multifamily Properties: These are often the workhorses of a real estate portfolio. Apartment buildings in places like Monterey or Salinas tend to have lower cap rates because the consistent demand for housing creates a reliable income stream, lowering the owner's risk. This stability is a huge reason why many choose to invest in income-producing properties.

- Retail and Commercial Spaces: You'll often see higher cap rates here to compensate investors for taking on more risk. A retail property's success is tied directly to the health of the economy and the tenant's business, making their income stream less predictable than an apartment rental.

- Single-Family Homes: High-end homes in premium spots like Pebble Beach typically have the lowest cap rates. For these properties, the investment strategy is not about immediate cash flow. It's about long-term appreciation and wealth preservation.

You can see these dynamics in the broader market. Rising borrowing costs have pushed cap rates up. In the U.S., multifamily housing cap rates climbed from a low of about 3.82% in 2021 to around 5.96% in 2023. Office properties, seen as riskier, jumped even higher, hitting an average of 6.54% by late 2023. You can dig into more data on how commercial property cap rates have changed to see these trends for yourself.

At the end of the day, this context is crucial for understanding how your investments are performing. By comparing your property’s cap rate to similar ones in the Monterey Bay Area, you get a much clearer, more honest picture of where it stands.

Making Smarter Investment Decisions with Cap Rate

Understanding your cap rate is one thing. Using it to drive your strategy is where the real value lies. For busy investors in Monterey County, this metric isn't just a number—it's a tool that helps you look forward, spot opportunities, and forecast returns with greater clarity. It’s about cutting through the noise and making decisions based on solid performance data.

For example, if you're looking at a property in Salinas with an unusually high cap rate compared to its neighbors, that could be a sign of an undervalued asset. On the flip side, a property with a cap rate far below the local average might be overvalued. This metric gives you a standardized way to compare an apartment building in Soledad to a commercial space in Monterey, helping you decide where your capital will work hardest.

A Holistic Approach to Investment Analysis

While powerful, the cap rate is just one piece of the puzzle. A sophisticated investment strategy always looks at the bigger picture. Cap rate is great for showing potential income relative to value, but it doesn't factor in financing or how much cash you actually invested.

For that reason, always consider it alongside other key metrics:

- Cash-on-Cash Return: This measures the annual pre-tax cash flow you receive relative to the actual cash you invested, giving you a clearer picture of your personal return.

- Total Return on Investment (ROI): This is the wide-angle lens. It looks at cash flow but also includes equity buildup from loan payments and the long-term appreciation of the property.

While cap rate shows potential return, the overall profitability of an investment property is heavily influenced by taxes. For a deeper look, check out this comprehensive Ultimate Guide to Taxes on Investment Property.

How Professional Management Boosts Your Bottom Line

So, what’s the most direct way to improve your property’s performance and long-term value? It all comes down to your Net Operating Income (NOI). When you increase your NOI, you don't just improve your cap rate—you directly increase the market value of your asset. This is where expert property management becomes a powerful lever for growth.

A key benchmark for understanding what is considered a good capitalization rate is comparing it to risk-free investments. Historically, multifamily real estate cap rates have averaged about 2.15% higher than the 10-year U.S. Treasury yield, rewarding investors for the added risks of property ownership.

At Coast & Valley, our entire focus is on optimizing your NOI to save you time and maximize your returns. We minimize vacancies, secure high-quality tenants at top market rates, and manage operating expenses with a professional eye. By improving NOI through strategic management and helping you understand all the available tax deductions for landlords, we enhance your property’s value and secure a stronger return on your investment.

Taking Your Property's ROI to the Next Level

Knowing your cap rate is one thing, but actively improving it is where you build real wealth. For property owners here in Monterey County, that number isn't just a static metric—it's a living indicator of your investment's health and a roadmap for what to do next. Boosting your property's performance takes a solid plan and local expertise.

There's no single "good" cap rate that fits every property. It's a balance between risk and reward. A property in a stable area like Pebble Beach will have a different profile than one in a growth market like King City. The most direct path to a better cap rate is to increase your Net Operating Income (NOI). When your NOI goes up, your property's value follows.

A Clear Path to a Stronger Portfolio

Getting a better cap rate and a healthier return requires a focused strategy. This is where professional management provides trust, transparency, and time-saving solutions.

Here’s our step-by-step approach to improving your property's performance:

- Step 1: Smart Rent Optimization. We conduct detailed market analyses to price your property for its maximum rental value without deterring quality tenants.

- Step 2: Proactive Expense Control. We keep costs in check by implementing preventive maintenance and using our network of trusted local vendors. This is about spending smart to protect your bottom line and preserve your asset.

- Step 3: Minimizing Vacancies. An empty unit is a liability. Our expert marketing and rigorous tenant screening find high-quality, long-term tenants who provide a steady, reliable income stream.

"Working with Amy Salmina and the Coast & Valley team completely changed how we viewed our investment. They didn't just manage the property; they found real opportunities to increase its value and boost our returns in ways we never would have seen on our own." – A Monterey County Property Investor

As a fourth-generation Salinas native with deep local roots, Amy Salmina offers an understanding of the Monterey County real estate landscape you can't get anywhere else. At Coast & Valley, we are your trusted advisors, dedicated to protecting your high-end assets and helping you achieve your financial goals.

Ready to see what your investment is truly capable of? Let our team provide a professional evaluation of your property. Contact Coast & Valley today for a comprehensive assessment and see how expert management can unlock your portfolio's true potential.

Answering Your Questions About Cap Rates

Even experienced investors have questions. Here are answers to some of the most common ones we hear about capitalization rates in the Monterey County market.

Is a Higher Cap Rate Always Better?

Not always. It's a classic risk vs. reward trade-off. While a higher cap rate suggests better immediate cash flow, it often signals higher risk.

For example, a lower cap rate in a stable market like Carmel might mean less cash flow each month, but it usually comes with greater long-term appreciation and security. A higher rate in an up-and-coming area could put more income in your pocket now, but you might face more market uncertainty or demanding management needs. The "better" rate is the one that fits your personal investment strategy and goals.

How Can a Property Manager Improve My Cap Rate?

A professional property manager is your key to boosting your cap rate because they directly influence your Net Operating Income (NOI). When your NOI goes up, your cap rate improves.

Here’s the action plan:

- Rent Optimization: We analyze local market data to set the highest possible rent that still attracts top-tier tenants for your property.

- Vacancy Minimization: An empty unit costs you money. We use expert marketing and a rigorous tenant screening process to keep your property filled with reliable renters who pay on time.

- Expense Control: We use our network of trusted local vendors and proactive maintenance to keep operational costs down without ever sacrificing quality or compliance.

Every dollar added to your NOI not only improves your cap rate but also directly increases your property's overall value, reinforcing trust in your investment's performance.

Can a Cap Rate Be Negative?

Yes, but it’s a major red flag. A negative cap rate means the property's annual operating expenses are higher than the gross income it brings in.

Essentially, the investment is losing money. This situation requires immediate attention, whether that means cutting costs, finding ways to boost revenue, or both. To truly understand your property's ROI, it's also critical to delve into investor loan interest rates and see how they impact your bottom line.

How Often Should I Recalculate My Cap Rate?

You should check your property's cap rate at least once a year. It's also smart to run the numbers again whenever something significant happens.

This could be a major change to your income or expenses, the completion of a large renovation, or a noticeable shift in property values in your specific Monterey County neighborhood. Staying on top of this metric keeps you in control and allows you to make timely, informed decisions.

Ready to unlock your property's full potential? The experts at Coast & Valley Properties can provide a comprehensive performance evaluation to identify opportunities for increasing your NOI and maximizing your return on investment. Contact us today to get started.